Florida won't stop rising insurance rates without combating climate change

Gov. Ron DeSantis and the Florida Legislature probably won't do anything about climate change this week. But it's a big reason insurance prices are going up.

This is Seeking Rents, a newsletter devoted to producing original journalism — and lifting up the journalism of others — that examines the many ways that businesses influence public policy across Florida, written by Jason Garcia.

From its headquarters in Zurich, Switzerland, Chubb Ltd. runs one of the largest insurance conglomerates in the world. The multinational giant, which has $200 billion in assets, sells both property insurance to wealthy homeowners, high-rise condos and commercial businesses and catastrophe reinsurance to other property insurers, including in Florida.

Like other insurers, Chubb has been raising prices for its property insurance products by double-digit percentages in recent months. But while insurance industry lobbyists in Florida have sought to blame soaring rates on frivolous claims and lawsuits churned out by unscrupulous roofers and lawyers, Chubb recently cited a different factor.

“Part of that is a reflection of revised views, given climate change,” Chubb Chairman and CEO Evan Greenberg told investment analysts during a company earnings call last month. “And that is pretty universally recognized by good underwriters in model changes that drive inflation and loss cost.”

Florida lawmakers return to the Capitol today, summoned by Gov. Ron DeSantis to Tallahassee where they will spend the week trying to stabilize a troubled insurance market in which some insurance companies are collapsing and others are jacking up prices or canceling policies altogether.

Legislative leaders recently unveiled package of changes that focus heavily on making it more difficult to sue insurance companies and slashing the fees attorneys can earn in insurance lawsuits, which would deter them from taking on such cases.

The package would also offer more publicly subsidized reinsurance, which is insurance that insurance companies buy and is a major driver of rising rates. Expanding public reinsurance is the easiest way to bring prices down for Florida home- and business owners without secretly making them pay for it in the form of lesser coverage or fewer legal rights. (Although one red flag: Legislative leaders have chosen to impose restrictions on this extra public reinsurance — which sure seems to have pleased lobbyists for the private reinsurance industry.)

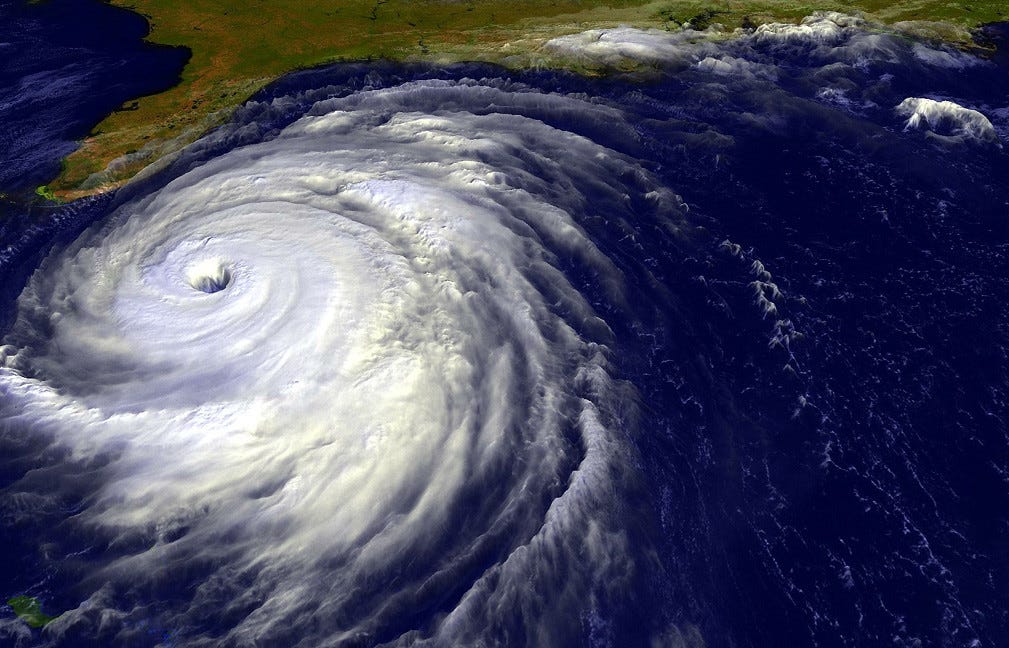

But what you won’t find in the Legislature’s reform package is anything to combat climate change. And as the commentary from Chubb shows, insurance costs are going to continue rising in Florida — a 450-mile peninsula jutting out into a rising Atlantic Ocean — without taking steps to combat the climbing temperatures and sea levels that generate more intense and more frequent storms and flooding.

Chubb is even more explicit in its regulatory filings. The company wrote in its most recent annual report that it is now “continually” adjusting its underwriting process — and its rates — to account for the impact of a warming climate, rising seas and more frequent hurricanes.

“Based on science and our own experience to date, we have conducted extensive work to understand the potential impact of climate change on our risk profile,” Chubb added. “These findings actively inform our underwriting risk appetite for property-related exposures for wild-fire, where we have significantly reduced our business in certain western states, and other perils such as flood and hurricane.

And Chubb is not alone.

“Anthropogenic climate change is both an existential threat to the planet and an imminent risk to our industry,” Kevin O’Donnell, the president and CEO of Bermuda-based reinsurance giant RenaissanceRe Holdings Ltd., said earlier this month.

Renaissance — which is partially owned by State Farm and sells reinsurance in Florida — said it recently revised its internal North American hurricane model in part to reflect the increased risk of storms due to climate change.

“We have been progressively integrating the consideration of the financial risk of climate change into our governance frameworks, risk management processes, and business strategies over the past several years,” the company added in a recent report to investors.

Renaissance also says there has been a “market trend shift away from property catastrophe risk due to the effects of climate change, social and monetary inflation, as well as a lack of confidence in catastrophe modeling.”

Meanwhile, Axis Capital Holdings Ltd., another major reinsurer, warned in a recent investor filing that the “frequency of severe weather-related events” has indisputably increased in recent years due to climate change.

“Climate change is likely to expose us to an increased frequency and/or severity of these weather-related losses, and there is a risk that our pricing of these perils or our management of the associated aggregations does not appropriately allow for changes in climate,” the company added. “Over the longer term, climate change may have an impact on the economic viability of certain lines of business if suitable adjustments in price and coverage cannot be achieved.”

Climate change has become a major problem for front-line insurance companies, too. New York-based insurance giant The Traveler’s Companies Inc. has sought to reassure its investors that it can shield itself from climate change-related losses because most of the policies it sells must be renewed annually — meaning the company can raise rates or slash coverage as needed to compensate for the impact of climate change.

Travelers also says it has been hiring more experts in data science, meteorology, geophysics and environmental engineering to help it better model the future impacts of climate change. “These results have been incorporated into the company’s product development, risk selection, pricing, capital allocation and claim response,” the company wrote in a recent investor filing.

“Climate change is a hard one to think about in any given period because you think about weather patterns over a long period of time. But clearly, if you just look at four of the last five years, our cat [catastrophe] experience was worse than what we would have expected,” Travelers Chairman and CEO Alan Schnitzer added during a company earnings call in January. “There's all sorts of things that are contributing to that. But we do see weather patterns, and we do take weather patterns into account in our loss pace and our pricing.”

Of course, particularly when it comes to climate change, it’s a lot easier to diagnose the problem than to fix it.

One of the most promising provisions in the bills that DeSantis and the Legislature are expected to pass this week would resurrect a grant program that is supposed to help Florida homeowners strengthen their homes against hurricane damage, through improvements such stronger roof tie-downs, secondary water-intrusion barriers, impact-resistant windows and hurricane-strength roofing shingles.

Florida leaders created the program in 2006, after seven hurricanes struck the state over two years between 2004 and 2005. But it’s been more than a decade since they actually funded it.

The insurance package lawmakers are expected to vote on this week would restart the program with $150 million in new funding. It would also expand the grants to cover homes valued at up to $500,000 (up from a previous cap of $300,000) and provide $2 in state funds for every $1 spent by the homeowner (up from a previous dollar-for-dollar match).

But mitigation is only part of the battle. To truly address climate change, Florida — which is, by itself, the world’s 15th largest economy — will have to wean itself off carbon-producing fossil fuels like coal and natural gas.

And DeSantis and the Florida Legislature have so far shown little interest in doing anything substantive to curtail greenhouse-gas emissions.

Just this past session, Republicans in the Florida House blocked a seemingly benign proposal that would have had the state’s newly created “chief resiliency officer” simply study options to reduce greenhouse-gas emissions. And last year DeSantis signed a bill written by natural-gas industry lobbyists that prevents cities and counties from passing local laws that try to limit the use of natural gas.

It’s a testament to the political influence of Florida’s utility companies, which currently generate less than 5 percent of their electricity from renewable energy sources — and particularly the state’s largest utility, Florida Power & Light, which is one of the biggest campaign contributors in all of Florida politics, doesn’t have plan to ever get to 100 percent renewable energy, and has fought to slow the spread of rooftop solar panels.

Exactly what is a state governor and legislature supposed to do about climate change? Go talk to China and India of you want to reduce emissions on climate change, The US has reduced emissions to a point we can't manufacture anything here. Oh by the way, China and India do not pay an ounce of attention to climate changers

Saying "Climate change is an Existential Threat to the planet" is just more Fear Porn nonsense, this guy destroyed his credibility with that statement. Interesting how the people making these claims like buying multi-$million beachfront mansions and have perfectly good nuclear power plants shutdown and replaced with coal & gas, while promoting nutty wind & solar scams that have done zip to alleviate GHG emissions apart from causing energy poverty.